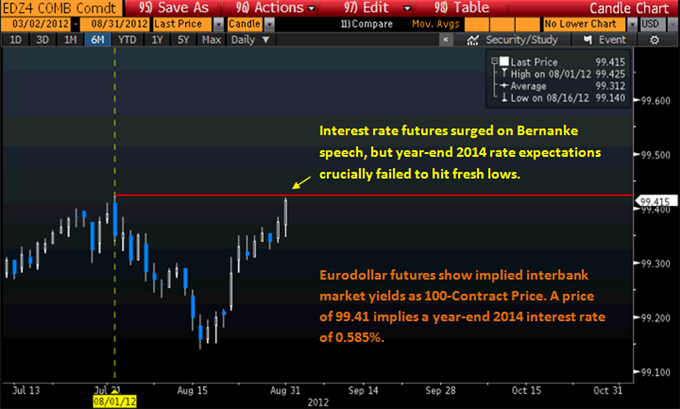

Fed Chairman Ben Bernanke sent the US Dollar (ticker: USDOLLAR) sharply higher and the US S&P 500 notably lower as he failed to provide clear indication that the Fed would institute the next wave of Quantitative Easing (QE3).

Bernanke critically said that the central bank “wouldn’t rule out further asset purchases” as stagnation in the US labor market remains a “grave concern”. Yet his words added little to recent Fed rhetoric which made clear that officials kept all options on the table—including further asset purchases.

US Dollar Surges as Bernanke Fails to Announce QE3, Dow Jones FXCM Dollar Index Sharply Higher

Thus the US Federal Reserve remains in “wait and see” mode as it keeps an especially close eye on domestic economic data. Bernanke himself said that the impact of Quantitative Easing has been “economically meaningful” as it helped drive long-term Treasury Bond yields significantly and added to a sustained recovery in US stock markets.

Yet ultimately the Fed’s moves have been far short of a panacea as the Fed Chairman highlighted labor market improvement as “painfully slow” and high unemployment could potentially “wreak structural damage” to the world’s largest economy.

The month of September looms large as a highly-anticipated US Nonfarm Payrolls report will shed further light on the state of the domestic labor market. Given the Fed’s clear focus on job creation, any significant disappointment in August Nonfarm Payrolls data could send the US Dollar sharply lower on expectations of further Federal Reserve Quantitative Easing.

Markets were on pins and needles ahead of Fed Chairman Ben Bernanke’s address as any surprises could force substantial swings across global financial markets. Bernanke famously used his 2010 speech at Jackson Hole to telegraph the Fed’s intention to institute the second wave of Quantitative Easing (QE2), and more recent Fed rhetoric suggested history could repeat itself with talk of QE3.

US Treasury Bonds traded sharply higher in the days ahead of Jackson Hole on the potential for further Quantitative Easing. Indeed, the 10-year Treasury Yield fell sharply off of a critical price ceiling at its 200-day Simple Moving Average—leaving the US Dollar itself at a critical juncture.

The next moves in the US Dollar could ultimately decide its trend through the rest of 2012 and set the tone for Greenback tracking into 2013.

ليست هناك تعليقات:

إرسال تعليق